Across thousands of communities around the world, savings groups continue to meet regularly to save money, issue loans, and support one another financially.

The model has proven remarkably resilient. For decades, groups have successfully managed collective savings using simple tools such as notebooks, handwritten ledgers, calculators, and lockboxes where cash is stored between meetings.

These systems have allowed millions of people to participate in financial activities even in places where formal banking infrastructure is limited.

But as savings groups expand in number and scale, the limitations of manual systems are becoming increasingly visible.

Many groups now manage complex financial activity—tracking member contributions, recording loans, calculating interest, and managing share-out distributions across entire savings cycles. When all of this information is recorded manually, maintaining accurate records can become difficult.

Paper ledgers can be lost or damaged. Calculations often need to be repeated several times to ensure accuracy. When groups issue multiple loans simultaneously, tracking repayment schedules manually can become time-consuming.

For organizations supporting hundreds or even thousands of savings groups, these challenges become even more significant. Collecting financial data from paper records can make it difficult to understand how groups are performing across different communities or identify where additional support may be needed.

As savings group networks continue to grow globally, these operational challenges are prompting new conversations about how community finance systems can be strengthened.

Digitization as the Next Step for Savings Groups

Digitization is increasingly emerging as a natural evolution of how savings groups manage their financial activities.

Instead of recording contributions, loans, and repayments in handwritten ledgers, groups can capture these transactions digitally. Contributions can be logged instantly, loan repayments can be tracked automatically, and calculations that once required careful manual work can be completed more efficiently.

Importantly, digitization does not change the core structure of savings groups. Members still meet regularly, discuss loan requests, and make financial decisions collectively.

What changes is how the information is recorded and managed. Digital systems make it possible to track savings group activity more consistently while preserving the community-driven nature of the model.

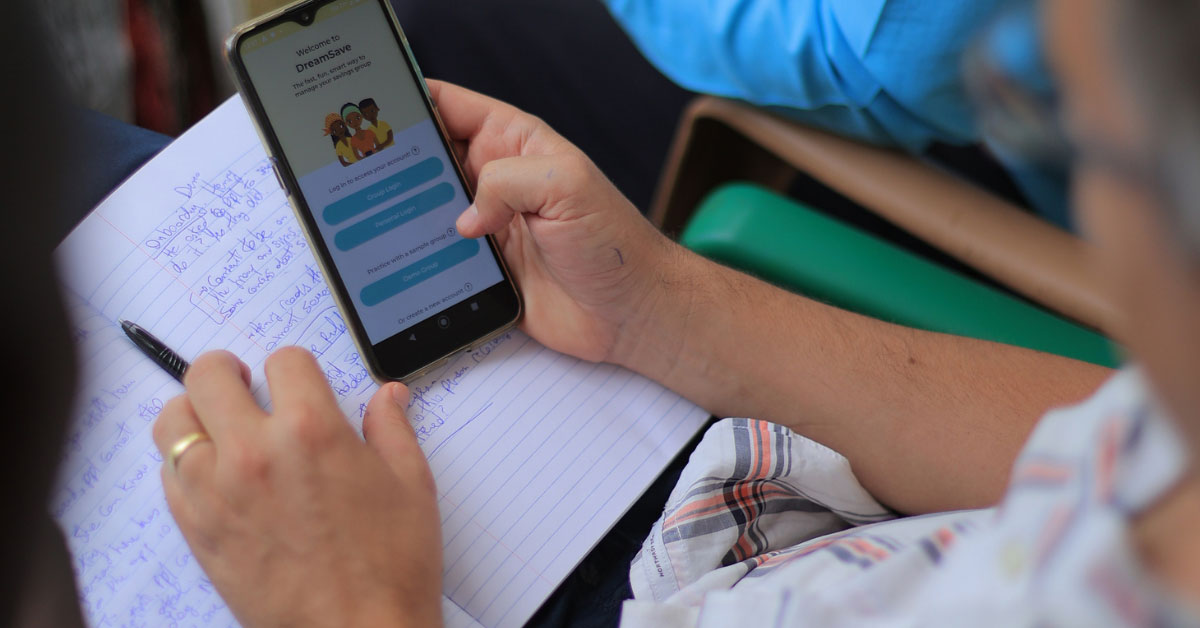

At DreamStart Labs, this thinking has informed the development of DreamSave, a platform designed specifically to support savings groups and the organizations that facilitate them.

Through DreamSave, savings groups can digitally record member contributions, track loans, monitor repayments, and manage share purchases during meetings. Instead of relying on paper ledgers, groups maintain structured financial records that are automatically calculated and securely stored.

This approach simplifies processes that can often be complex when managed manually. Calculations for loan balances, repayment schedules, and share-out distributions can be generated automatically based on group activity throughout the savings cycle.

For facilitators working directly with groups, digital tools can help streamline meeting processes, reduce time spent on manual calculations, and make it easier to review financial records with members during meetings.

Over time, these digital records also create something that many savings groups historically lacked: documented financial histories. When contributions, loans, and repayments are recorded consistently, savings groups begin to build verifiable financial data. This information helps demonstrate the savings behavior and repayment discipline that many groups already maintain, potentially strengthening their ability to engage with financial service providers.

In this way, digitization helps translate the financial activity already taking place within savings groups into information that can be recognized across the broader financial ecosystem.

Improving Visibility for Organizations Supporting Savings Groups

Digitization also changes how organizations support savings group programs.

When groups operate entirely through paper records, program teams often rely on periodic reports collected by field facilitators. This process can make it difficult to gain timely insights into how groups are performing across large networks.

Digital systems allow financial data to be captured more consistently and aggregated across entire programs.

Through DreamInsights, DreamStart Labs provides tools that allow organizations supporting savings groups to monitor performance across large networks of groups. Program teams can view data on savings contributions, loan activity, and repayment patterns, helping them identify trends and better understand how groups are progressing across different communities.

This visibility allows organizations to identify challenges earlier, provide targeted support to facilitators, and strengthen the design of savings group programs over time.

For initiatives supporting thousands of groups across multiple regions, access to structured data can significantly improve how programs are managed and evaluated.

Expanding Opportunities for Financial Access

Digitization also creates new opportunities for savings groups to connect with the broader financial system.

As groups build reliable financial records, it becomes easier to demonstrate their financial activity and discipline. These records can help support relationships with financial institutions offering services such as savings accounts, insurance products, or small business loans.

Digital platforms may also allow savings groups to integrate with mobile money systems, making it easier for members to deposit or withdraw funds electronically.

These connections help bridge the gap between community-based finance and formal financial services while allowing savings groups to maintain their independence and local governance.

Strengthening the Systems Communities Have Built

Savings groups have always evolved to meet the financial needs of their members. From traditional rotating savings systems to structured models such as Village Savings and Loan Associations, communities have adapted these systems over time.

Digitization represents another stage in that evolution. At DreamStart Labs, we work alongside partners supporting savings groups across multiple regions, helping strengthen the systems that enable these community-based financial networks to operate effectively.

Today, our technology supports more than 35,000 savings groups serving over 750,000 members, helping organizations manage savings group programs more efficiently while supporting the communities they serve.

Digital tools do not replace the trust, collaboration, and participation that define savings groups. Instead, they strengthen the systems that allow these community-driven financial networks to continue growing.

Understanding how digitization strengthens savings groups naturally leads to the next question: how can organizations introduce these tools successfully while preserving the trust and participation that make savings groups effective?